As we approach the first Quarter of 2024, inflation remains a top concern for consumers and businesses alike, while central banks pay lip service to ordinary people’s experiences on the ground. Despite a record-speed hiking cycle, inflation remains sticky. It sits above previous “expected rates” of debasement central banks had set as a tolerable spanking to those who generate economic value.

The fear that inflation has not been tamed and easing policy could drive up inflation rates faster than central banks and governments can tolerate results in what we’re hearing lately.

In order to stem any kind of inflation and get back to those rates of old, we must maintain these current interest rate hikes as long as possible despite the increased debt load and possible sector failures, like commercial real estate and parts of the banking world exposed to that type of real estate.

I am no economist, but how does slower inflation help me if it’s still compounding two previous years that had a massive increase? For example, if I had $100, it holds much less purchasing power today than spending it five years ago.

| Year | Inflation Rate | Purchasing Power |

|---|---|---|

| 2019 | $100 | |

| 2020 | 2,5% | $97.5 |

| 2021 | 1.4% | $96.13 |

| 2022 | 7.5% | $88.92 |

| 2023 | 6.4% | $83.22 |

If the previous year was, let’s say, a high inflation year of 6.4%, and this year it’s 2%, the loss in purchasing power stacks up despite the lower inflation rate. Now, this is all supposed to be smoothed out by your interest from your risk-free rate or whatever yield-bearing instruments you can access, but how much protection is that really offering the average person?

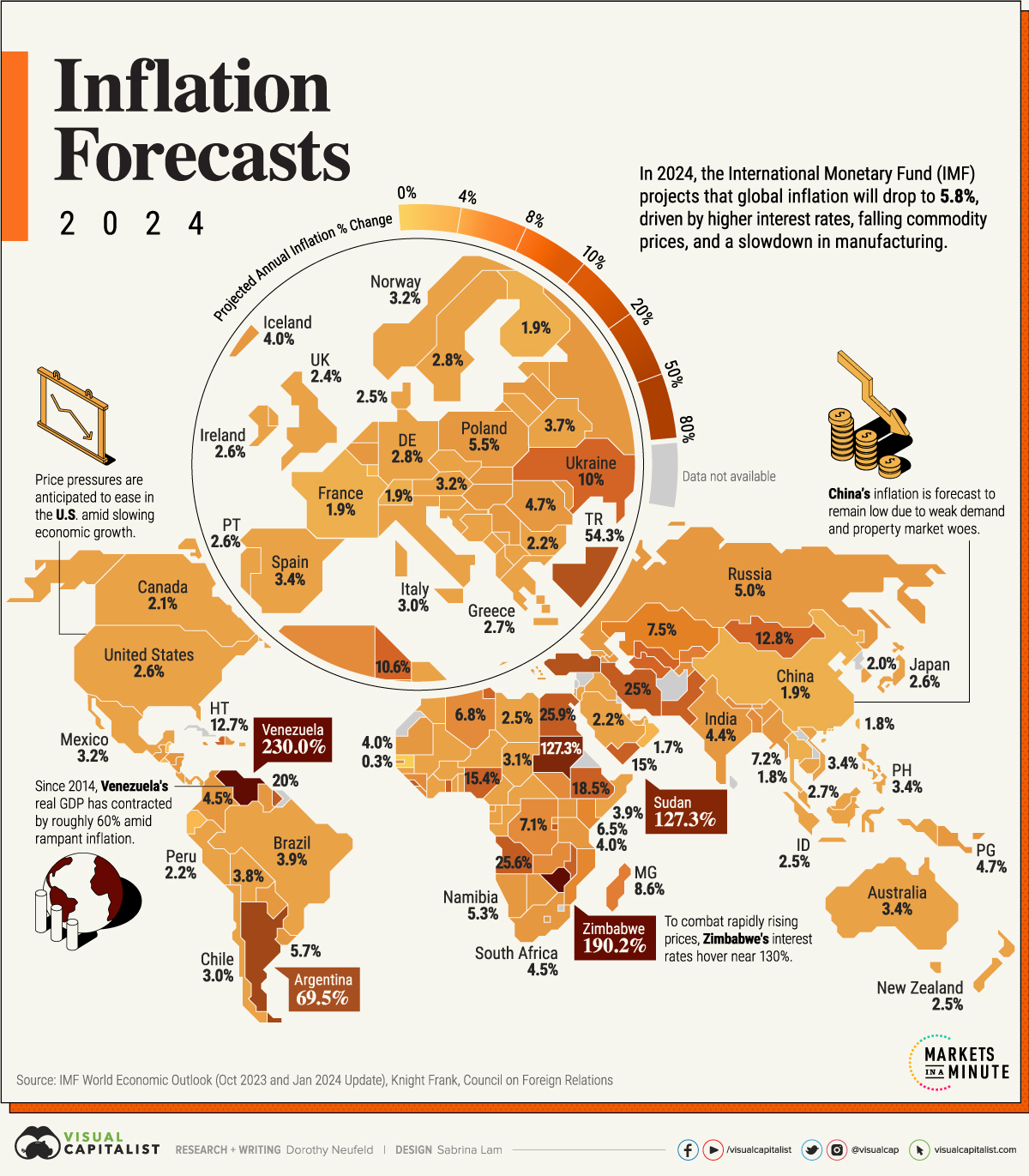

I recently saw this great chart from the Visual Capitalist, showcasing inflation rates per country. I thought it would be interesting to overlay it with proposed interest rates for each country per year to give us an idea of what your so-called real rates would be.

So, let’s examine the current economic climate and explore what we can expect from inflation in 2024.

Inflation rates, interest rates and real rates

Now, this is no gospel. Inflation figures can be backdated and changed, and inflation rate calculations are ALWAYS changing, being reworked and using different hedonic adjustments. Of course, interest rates can also change. All this table shows is an overview of what the expected rates of holding your local fiat currency could be like.

It’s worth noting that only some get these interest rates in their local currency; some do. Some can access better products yielding more, others worse products yielding less, and anyone sitting in cash—well, you take the full brunt of the debasement, and we thank you for your service.

What I found interesting was that 20 nations, despite their interest rate policies, are offering a negative return, regardless of the offsetting. Given that governments are prone to understating inflation, quite a few could be in this territory, too.

Another caveat that non-USD-based countries will also need to consider is the unexpected devaluation of a country’s currency to the US dollar.

This feat has become more common lately.

In the last few months alone, we’ve seen Argentina, Nigeria, and Egypt give up trying to maintain a price range for their local currencies against the dollar, allowing for market price discovery, and that’s never to the upside.

So, if you’re holding a currency that has gone through a devaluation, you’re likely deep in negative returns.

| Country | Projected Annual Inflation Change 2024 | 2024 Interest Rates | Projected Real Rates |

| 🇻🇪 Venezuela | 230,00% | 57,84% | -172,16% |

| 🇿🇼 Zimbabwe | 190,20% | 130% | -60,20% |

| 🇸🇩 Sudan | 127,30% | 28,30% | -99,00% |

| 🇦🇷 Argentina | 69,50% | 100% | 30,50% |

| 🇹🇷 Türkiye | 54,30% | 45% | -9,30% |

| 🇪🇬 Egypt | 25,90% | 21,25% | -4,65% |

| 🇦🇴 Angola | 25,60% | 18% | -7,60% |

| 🇮🇷 Iran | 25,00% | 23% | -2,00% |

| 🇧🇮 Burundi | 22,40% | 12% | -10,40% |

| 🇸🇱 Sierra Leone | 21,70% | 22,25% | 0,55% |

| 🇸🇷 Suriname | 20,00% | 10% | -10,00% |

| 🇪🇹 Ethiopia | 18,50% | 7% | -11,50% |

| 🇵🇰 Pakistan | 17,50% | 22% | 4,50% |

| 🇳🇬 Nigeria | 15,40% | 22,75% | 7,35% |

| 🇲🇼 Malawi | 15,20% | 26% | 10,80% |

| 🇬🇭 Ghana | 15,00% | 29% | 14,00% |

| 🇾🇪 Yemen | 15,00% | 27% | 12,00% |

| 🇲🇳 Mongolia | 12,80% | 13% | 0,20% |

| 🇭🇹 Haiti | 12,70% | 17% | 4,30% |

| 🇺🇿 Uzbekistan | 10,70% | 14% | 3,30% |

| 🇹🇳 Tunisia | 10,60% | 8% | -2,60% |

| 🇺🇦 Ukraine | 10,00% | 15% | 5,00% |

| 🇲🇬 Madagascar | 8,60% | 9,50% | 0,90% |

| 🇰🇬 Kyrgyz Republic | 8,00% | 13% | 5,00% |

| 🇿🇲 Zambia | 7,90% | 12,50% | 4,60% |

| 🇲🇺 Mauritius | 7,80% | 4,50% | -3,30% |

| 🇬🇳 Guinea | 7,80% | 11% | 3,20% |

| 🇰🇿 Kazakhstan | 7,50% | 14,75% | 7,25% |

| 🇧🇩 Bangladesh | 7,20% | 6,50% | -0,70% |

| 🇲🇲 Myanmar | 7,20% | 7% | -0,20% |

| 🇸🇹 São Tomé and Príncipe | 7,20% | 10% | 2,80% |

| 🇬🇲 The Gambia | 7,10% | 17% | 9,90% |

| 🇨🇩 Democratic Republic of the Congo | 7,10% | 25% | 17,90% |

| 🇩🇿 Algeria | 6,80% | 3% | -3,80% |

| 🇹🇯 Tajikistan | 6,50% | 9,50% | 3,00% |

| 🇳🇵 Nepal | 6,50% | 7% | 0,50% |

| 🇰🇪 Kenya | 6,50% | 13% | 6,50% |

| 🇲🇿 Mozambique | 6,50% | 16,50% | 10,00% |

| 🇸🇸 South Sudan | 6,10% | 12% | 5,90% |

| 🇱🇷 Liberia | 6,00% | 20% | 14,00% |

| 🇺🇾 Uruguay | 5,70% | 9% | 3,30% |

| 🇵🇱 Poland | 5,50% | 5,75% | 0,25% |

| 🇬🇾 Guyana | 5,50% | 5% | -0,50% |

| 🇷🇼 Rwanda | 5,50% | 7,50% | 2,00% |

| 🇭🇺 Hungary | 5,40% | 9% | 3,60% |

| 🇳🇦 Namibia | 5,30% | 7,75% | 2,45% |

| 🇬🇶 Equatorial Guinea | 5,20% | 5% | -0,20% |

| 🇧🇹 Bhutan | 5,10% | 6,85% | 1,75% |

| 🇦🇿 Azerbaijan | 5,00% | 7,75% | 2,75% |

| 🇯🇲 Jamaica | 5,00% | 7% | 2,00% |

| 🇱🇸 Lesotho | 5,00% | 7,75% | 2,75% |

| 🇲🇩 Moldova | 5,00% | 4,25% | -0,75% |

| 🇷🇺 Russia | 5,00% | 16% | 11,00% |

| 🇺🇬 Uganda | 5,00% | 9,50% | 4,50% |

| 🇳🇮 Nicaragua | 4,80% | 7% | 2,20% |

| 🇵🇬 Papua New Guinea | 4,70% | 2% | -2,70% |

| 🇷🇴 Romania | 4,70% | 7% | 2,30% |

| 🇬🇹 Guatemala | 4,60% | 5% | 0,40% |

| 🇿🇦 South Africa | 4,50% | 8,25% | 3,75% |

| 🇸🇰 Slovak Republic | 4,50% | 4,50% | 0,00% |

| 🇨🇴 Colombia | 4,50% | 12,75% | 8,25% |

| 🇮🇳 India | 4,40% | 6,50% | 2,10% |

| 🇧🇼 Botswana | 4,40% | 2,40% | -2,00% |

| 🇸🇿 Eswatini | 4,30% | 7,50% | 3,20% |

| 🇱🇻 Latvia | 4,30% | 4,50% | 0,20% |

| 🇭🇳 Honduras | 4,20% | 3% | -1,20% |

| 🇧🇪 Belgium | 4,00% | 4,50% | 0,50% |

| 🇮🇸 Iceland | 4,00% | 9,25% | 5,25% |

| 🇹🇿 Tanzania | 4,00% | 5,50% | 1,50% |

| 🇲🇷 Mauritania | 4,00% | 8% | 4,00% |

| 🇵🇾 Paraguay | 4,00% | 6,25% | 2,25% |

| 🇷🇸 Serbia | 4,00% | 6,50% | 2,50% |

| 🇩🇴 Dominican Republic | 4,00% | 7% | 3,00% |

| 🇦🇲 Armenia | 4,00% | 8,75% | 4,75% |

| 🇧🇷 Brazil | 3,90% | 11,25% | 7,35% |

| 🇧🇴 Bolivia | 3,80% | 3,50% | -0,30% |

| 🇧🇾 Belarus | 3,70% | 9,50% | 5,80% |

| 🇨🇲 Cameroon | 3,70% | 5% | 1,30% |

| 🇪🇪 Estonia | 3,60% | 4,50% | 0,90% |

| 🇧🇧 Barbados | 3,60% | 2% | -1,60% |

| 🇦🇱 Albania | 3,60% | 3,25% | -0,35% |

| 🇦🇺 Australia | 3,40% | 4,35% | 0,95% |

| 🇪🇸 Spain | 3,40% | 4,50% | 1,10% |

| 🇵🇭 Philippines | 3,40% | 6,50% | 3,10% |

| 🇻🇳 Vietnam | 3,40% | 4,50% | 1,10% |

| 🇲🇦 Morocco | 3,30% | 3% | -0,30% |

| 🇸🇮 Slovenia | 3,30% | 4,50% | 1,20% |

| 🇦🇹 Austria | 3,20% | 4,50% | 1,30% |

| 🇭🇷 Croatia | 3,20% | 4,50% | 1,30% |

| 🇨🇬 Republic of Congo | 3,20% | 5% | 1,80% |

| 🇲🇽 Mexico | 3,20% | 11,25% | 8,05% |

| 🇳🇴 Norway | 3,20% | 4,50% | 1,30% |

| 🇸🇬 Singapore | 3,20% | 3,75% | 0,55% |

| 🇱🇹 Lithuania | 3,10% | 4,50% | 1,40% |

| 🇲🇪 Montenegro | 3,10% | 4,50% | 1,40% |

| 🇹🇩 Chad | 3,10% | 5% | 1,90% |

| 🇨🇱 Chile | 3,00% | 7,25% | 4,25% |

| 🇨🇷 Costa Rica | 3,00% | 5,75% | 2,75% |

| 🇬🇪 Georgia | 3,00% | 9% | 6,00% |

| 🇬🇼 Guinea-Bissau | 3,00% | 5,50% | 2,50% |

| 🇮🇶 Iraq | 3,00% | 7,50% | 4,50% |

| 🇮🇹 Italy | 3,00% | 4,50% | 1,50% |

| 🇰🇭 Cambodia | 3,00% | 0,83% | -2,17% |

| 🇱🇦 Lao P.D.R. | 3,00% | 7,50% | 4,50% |

| 🇩🇪 Germany | 2,80% | 4,50% | 1,70% |

| 🇸🇪 Sweden | 2,80% | 4% | 1,20% |

| 🇬🇷 Greece | 2,70% | 4,50% | 1,80% |

| 🇲🇾 Malaysia | 2,70% | 3% | 0,30% |

| 🇧🇸 The Bahamas | 2,60% | 4% | 1,40% |

| 🇮🇪 Ireland | 2,60% | 4,50% | 1,90% |

| 🇮🇱 Israel | 2,60% | 4,50% | 1,90% |

| 🇯🇴 Jordan | 2,60% | 7,50% | 4,90% |

| 🇯🇵 Japan | 2,60% | -0,10% | -2,70% |

| 🇵🇹 Portugal | 2,60% | 4,50% | 1,90% |

| 🇺🇸 United States | 2,60% | 5,50% | 2,90% |

| 🇧🇯 Benin | 2,50% | 5,50% | 3,00% |

| 🇨🇫 Central African Republic | 2,50% | 5% | 2,50% |

| 🇩🇰 Denmark | 2,50% | 3,60% | 1,10% |

| 🇮🇩 Indonesia | 2,50% | 6% | 3,50% |

| 🇱🇾 Libya | 2,50% | 3% | 0,50% |

| 🇳🇪 Niger | 2,50% | 5,50% | 3,00% |

| 🇳🇿 New Zealand | 2,50% | 5,50% | 3,00% |

| 🇬🇦 Gabon | 2,40% | 5% | 2,60% |

| 🇬🇧 United Kingdom | 2,40% | 5,25% | 2,85% |

| 🇲🇹 Malta | 2,40% | 4,50% | 2,10% |

| 🇲🇻 Maldives | 2,40% | 7% | 4,60% |

| 🇳🇱 Netherlands | 2,40% | 4,50% | 2,10% |

| 🇸🇨 Seychelles | 2,40% | 2% | -0,40% |

| 🇦🇪 UAE | 2,30% | 5,40% | 3,10% |

| 🇭🇰 Hong Kong SAR | 2,30% | 5,75% | 3,45% |

| 🇲🇰 North Macedonia | 2,30% | 6,30% | 4,00% |

| 🇶🇦 Qatar | 2,30% | 6,25% | 3,95% |

| 🇹🇹 Trinidad and Tobago | 2,30% | 3,50% | 1,20% |

| 🇧🇬 Bulgaria | 2,20% | 3,80% | 1,60% |

| 🇨🇾 Cyprus | 2,20% | 4,50% | 2,30% |

| 🇨🇿 Czech Republic | 2,20% | 6,25% | 4,05% |

| 🇵🇦 Panama | 2,20% | 2,14% | -0,06% |

| 🇵🇪 Peru | 2,20% | 6,25% | 4,05% |

| 🇸🇦 Saudi Arabia | 2,20% | 6% | 3,80% |

| 🇹🇬 Togo | 2,20% | 5,50% | 3,30% |

| 🇧🇦 Bosnia and Herzegovina | 2,10% | 4,30% | 2,20% |

| 🇨🇦 Canada | 2,10% | 5% | 2,90% |

| 🇱🇨 St. Lucia | 2,10% | 1,23% | -0,87% |

| 🇧🇫 Burkina Faso | 2,00% | 5,50% | 3,50% |

| 🇨🇮 Côte d’Ivoire | 2,00% | 5,50% | 3,50% |

| 🇨🇻 Cabo Verde | 2,00% | 1,25% | -0,75% |

| 🇰🇷 Korea | 2,00% | 3,50% | 1,50% |

| 🇲🇱 Mali | 2,00% | 5,50% | 3,50% |

| 🇨🇭 Switzerland | 1,90% | 1,75% | -0,15% |

| 🇨🇳 China | 1,90% | 3,45% | 1,55% |

| 🇫🇮 Finland | 1,90% | 4,50% | 2,60% |

| 🇫🇷 France | 1,90% | 4,50% | 2,60% |

| 🇹🇭 Thailand | 1,80% | 2,50% | 0,70% |

| 🇹🇼 Taiwan | 1,80% | 1,88% | 0,08% |

| 🇱🇺 Luxembourg | 1,70% | 4,50% | 2,80% |

| 🇲🇴 Macao SAR | 1,70% | 5,75% | 4,05% |

| 🇴🇲 Oman | 1,70% | 6% | 4,30% |

| 🇸🇻 El Salvador | 1,70% | 5,02% | 3,32% |

| 🇰🇲 Comoros | 1,60% | 3,08% | 1,48% |

| 🇧🇳 Brunei Darussalam | 1,50% | 5,50% | 4,00% |

| 🇪🇨 Ecuador | 1,50% | 10,14% | 8,64% |

| 🇧🇭 Bahrain | 1,40% | 6,25% | 4,85% |

| 🇧🇿 Belize | 1,20% | 2,25% | 1,05% |

| 🇸🇳 Senegal | 0,30% | 5,50% | 5,20% |

A Look Back: 2023’s Inflationary Pressures

2023 witnessed a continuation of the inflationary trends that began after the “Global Reopening. As people got their stimmys from government programs and could move around, eat, travel and go to public gatherings, they began to spend.

That spending put pressure on Just In Time supply chains, and we saw massive backlogs in international shipping. If you take a bunch of capacity offline, it takes a while to ramp back up and needs constant demand to validate ramping up, or you leave yourself exposed to overinvesting in something that was a short-term trend and see yourself going out of business.

Then, you can add factors like supply chain disruptions, blowing up pipelines and forcing the EU to look at other energy markets, the war in Ukraine, and ongoing labour shortages, as well as the BRICS versus NATO trade block competition, which all contributed to rising prices across various sectors.

Central banks worldwide don’t have the tools to deal with what is happening in the physical world as much as they pretend to tell us they do, so they have to respond with the tools by raising interest rates to curb inflation. Even if that inflation isn’t driven by monetary or fiscal policy and is geopolitical in nature, it doesn’t matter; inflation is up, so tightening is all central banks can do.

What’s on the Horizon for 2024?

Predicting the future of inflation is always a complex task, and no one knows the answer; as much as we want them to, the only known monetary policy in the world is reserved for Bitcoin. However, here are some factors that could influence inflation in 2024:

- Monetary Policy: The world’s central banks’ continuing or maintaining interest rate hikes are expected to dampen inflation as borrowing becomes more expensive. However, these measures’ effectiveness and lag time still need to be determined.

- Global Supply Chains: Normalising global supply chains could alleviate some price pressures, but ongoing geopolitical tensions pose risks.

- Energy Prices: Fluctuations in global energy prices, particularly oil and gas, can significantly impact inflation as they affect transportation costs and production processes.

- Consumer Behaviour: Consumer spending patterns will play a crucial role. Inflationary pressures could ease if spending continues to decline in response to rising prices.

- Rate hike weakening effects: Rate hikes don’t mean people will respond exactly as you predict, which is evident in how the stock markets are ripping despite higher borrowing costs. What might have felt like Goku trading under 100 times Earth gravity becomes the norm, and markets acclimate to them.

Forecasts are not fortune-telling, but fortunes can be lost on them

Economic experts hold varying opinions on the trajectory of inflation in 2024. Some predict a gradual decline as the impact of monetary policy takes hold. Others warn that inflation could remain stubbornly high if global factors like the war in Ukraine persist.

Additionally, war in the Middle East and the resulting disruption in the region’s supply chains could also contribute to demand meeting supply and requiring prices to adjust upwards to compensate.

Another concern is that we have no idea what is coming down the pike; so far, in Q1 of 2024, we saw New York Community Bank get a bailout in exchange for equity and even Jerome Powell, the Fed chair, claimed more banks could fail.

What can you do?

While the future of inflation remains uncertain, you, as a citizen, don’t have any more tools in your arsenal than in previous years. For an increasing number of people, using them becomes even more challenging.

These principles remain applicable because they work; now, if you’re cash flow is just enough to keep a tent over your head, then we’re not solving that issue overnight, but for those who are feeling the pinch of inflation and have resources to do something about it, it’s never too late to start an action plan.

- Spend less than you make: Review your budget, analyse your spending habits, and identify areas where you can cut back to offset rising costs.

- Increase your income or relative buying power: This isn’t easy or applicable to most people but, if possible, should be entertained; first is to fight for that raise or start moving around to get a better market rate for your services, increase your prices for your services to compensate and force the inflation on the next sucker. For those who are in the remote work sector, downscaling from a neighbourhood or even to a country with a cheaper cost of living can be an option for some willing to deal with all that drama.

- Invest in assets that hedge against inflation: Consider investments that play to your strength and knowledge, like real estate or certain commodities such as gold, which are historically known to hold their value during inflationary periods. These assets are great if you don’t have an alternative like Bitcoin, which has continued to outpace inflation and provide outsized returns for over a decade, but I leave the choice up to you.

I am not here to tell you Bitcoin is the panacea and answer to all your inflation worries; its effect on your life will depend on your country, time frame, income and future ability to defer income, so there are plenty of variables to consider.

Yes, Bitcoin is volatile, but as you compare it to the ever-increasing volatility of your local currency, consider having a foot in both ecosystems and start to allocate based on the one that rewards you best.

Don’t trust a random blogger on the internet; do the experiment for yourself and see if it works. If you can save $100 a month, do it. Let’s say you split 50/50 for simplicity’s sake into a savings account and the other half into Bitcoin. Just see which one has given you a better return over the year, two years, or three years, and adjust based on what you feel works for you and what you feel comfortable with holding in each ecosystem.

Drop us a real-time inflation print

So, how are you dealing with inflation in your part of the world? Do the figures above reflect what you’re seeing on the ground? Let us know in the comments down below.