Bitcoiner and Bank to the Future co-founder Simon Dixon has issued one of his most urgent warnings yet: we are entering what he calls “the Wall Street attack phase”—a systematic effort by institutional finance to pull your Bitcoin into custodial wrappers and, in times of crisis, separate you from your coins permanently.

While Michael Saylor and MicroStrategy (now Strategy) are celebrated as financial engineering heroes and pioneers in bringing Bitcoin to traditional capital markets, accumulating over 649,000 BTC in the process and inspiring dozens of copycats

“Bitcoin treasury companies” might not be the next step in stacking, but at best, they are another paper product with a misplaced risk profile. And at its worst, it’s a sophisticated trap designed to recreate the same counterparty risks, leverage cascades, and wealth extraction mechanisms that Bitcoin was created to escape.

This isn’t theoretical.

As of November 2025, Strategy stock has fallen 40% in the past month as Bitcoin has lost around 30% of its value since October 2025. JPMorgan warns of $8.8 billion in forced selling if the company gets delisted from major indices, and the entire Bitcoin treasury company model is showing its first serious cracks.

We’ve already seen fellow treasury company Kindly MD Inc. (Naka) begin to crack. The company’s stock is down (-85.33%), trading at 44 cents, down from its all-time high of $22.60 and has already been forced to sell 367 BTC, worth $35 million, to keep itself afloat.

The question Dixon poses is stark: Are you holding Bitcoin, or are you holding an IOU that Wall Street can seize when the music stops?

What Are Bitcoin Treasury Companies?

Bitcoin treasury companies represent a new corporate structure that has exploded in popularity since MicroStrategy’s pioneering move in August 2020. The concept is deceptively simple: rather than holding traditional treasury assets like cash, bonds, or equities, these companies hold Bitcoin as their primary reserve asset.

The model works like this: Companies raise capital through debt issuance (convertible bonds, notes) and equity offerings (stock sales, preferred shares), then use those proceeds to buy Bitcoin. The bet is that Bitcoin appreciates faster than the cost of debt, creating a positive carry that benefits shareholders through leveraged exposure to Bitcoin’s price movement.

The strategy’s success has been remarkable.

Since 2020, the company has increased its market value over twentyfold to more than $100 billion—exceeding established financial institutions like State Street. As of late 2025, Strategy holds 649,870 Bitcoin purchased at an average price of $74,433, representing approximately 2.7% of Bitcoin’s total supply.

The model has spawned imitators worldwide: Metaplanet in Japan, the Smarter Web Company in the UK, Semler Scientific, MARA Holdings, and dozens more, with direct listings and even SPACs coming to market in the US.

It’s been a crazy year for Bitcoin treasury companies. Apart from the AI pivot, it has been the biggest narrative in drumming up shareholder interest in recent years.

We’ve even seen treasury companies pop up in the South African and Namibian stock markets. These companies are hoping that being the first mover in their local market will position them as the premier asset for Bitcoin exposure for local capital flows.

Currently, Bitcoin treasury companies account for one-fourth of all publicly traded companies holding Bitcoin. Start-ups in marketing, education, and software development have largely abandoned their original business models to bet everything on Bitcoin.

If that doesn’t make your hair stand up on end, you’re probably not well or well-versed in the risk.

For traditional investors, the appeal is: indirect exposure to Bitcoin with built-in leverage, tax advantages in certain jurisdictions, regulatory workaround access to crypto where direct investment faces restrictions, and the ability to hold Bitcoin exposure in traditional brokerage accounts alongside stocks and bonds.

Simon Dixon’s Warning: The Two-Tier System Emerging

In his interviews with Bitcoin Archive’s Archie and on his #BitcoinHardTalk platform, Dixon characterises the current moment as the culmination of a 14-year series of attacks on Bitcoin—from exchange failures to regulatory squeezes—now reaching its most sophisticated phase.

“People underestimate what Wall Street is willing to do to take your Bitcoin,” Dixon warns.

He describes an emerging two-tier system: Bitcoin held in Wall Street custody through ETFs, pensions, corporate treasuries, and Bitcoin-backed loans versus Bitcoin held in self-custody. The former represents what Dixon calls “Bitcoin IOUs”—claims on Bitcoin rather than actual Bitcoin ownership—while the latter represents true property you can own and control.

Dixon’s thesis is that institutional finance is assembling the plumbing and incentives to pull customer coins into custodial wrappers and, in crisis situations, separate investors from their Bitcoin through bankruptcy proceedings, margin liquidations, and forced selling events.

“Bitcoin is money you can own, money you can spend, and money that has a fixed supply with a monetary policy that nobody can change,” Dixon emphasises.

But Bitcoin held through treasury companies, ETFs, and custodial platforms loses these essential properties, becoming indistinguishable from traditional financial assets subject to counterparty risk, leverage cascades, and institutional control.

The Seven Critical Risks of Bitcoin Treasury Companies

Based on Simon Dixon’s analysis and recent market developments, Bitcoin treasury companies introduce multiple layers of risk that self-custody eliminates entirely:

1. Leverage and Margin Cascade Risk

The most immediate danger Dixon identifies is the interconnected web of leverage that treasury companies create. While proponents argue that corporate debt with long maturities is fundamentally different from the margin trading and rehypothecation that destroyed platforms like Celsius and BlockFi in 2022, Dixon counters that the real risk emerges when individually sensible structures are linked into a pipeline.

The system works like this: ETFs and index funds direct flows into treasury company stocks, those companies issue corporate debt denominated in fiat with dividend commitments, stablecoin credit interlaces with Bitcoin-backed loans, distressed buyouts roll assets into the largest public vehicles, and mining equities sit inside the same index-fund complex. “When you combine all of these different products together, you can then do this margin process,” Dixon explains.

The scenario he sketches is chilling: A severe Bitcoin drawdown triggers margin calls on leveraged positions, treasury company stocks plummet faster than Bitcoin itself (amplifying losses through their leverage), bankruptcy proceedings begin as companies can’t service debt obligations, and custodial honeypots concentrate even more coins into fewer hands.

In addition, you might not have complete oversight of the claims on that underlying Bitcoin, as the proof of liabilities might not be clear or deliberately kept opaque.

Strategy’s recent performance validates this concern. While Bitcoin fell roughly 8% year-to-date as of November 2025, Strategy stock has fallen 39%—nearly five times Bitcoin’s decline. During the past month, Strategy dropped 40% while Bitcoin remained relatively stable. This volatility amplification is a feature of leveraged structures, not a bug, and it demonstrates how treasury companies magnify downside risk.

“All you need to do to protect yourself when that event happens is own Bitcoin in self-custody,” Dixon states simply.

2. Counterparty Risk: The CEO, The Custodian, The Brokerage

Dixon draws a crucial distinction between Bitcoin’s promise and treasury company reality. Michael Saylor himself frequently emphasises that Bitcoin offers “absolute freedom from counterparty risk,” operating independently of governments, corporations, and cultural dynamics. “No company. No country. No creditor. No currency. No competitor. No culture. Not even chaos,” Saylor declares.

But here’s the irony Dixon identifies: when you buy shares in Strategy or any Bitcoin treasury company, you’ve just introduced three layers of counterparty risk:

- The CEO and Management: Your investment depends entirely on management decisions. Will they continue the Bitcoin strategy, or pivot? Will they sell Bitcoin at inopportune times? Will they take on more leverage? Michael Saylor’s outsized control over Strategy means shareholders are betting on one person’s judgment and continued commitment to the Bitcoin thesis.

- The Custodian: Treasury companies don’t self-custody their Bitcoin—they use institutional custodians like Coinbase, Fidelity, or BitGo. Your ownership claim depends on the custodian maintaining proper segregation, avoiding bankruptcy, resisting government pressure, and not being hacked. Recent revelations about Strategy’s wallet addresses being exposed raise operational security concerns that self-custody eliminates.

- The Brokerage: You don’t even directly own treasury company shares—your brokerage does, on your behalf. In crisis scenarios, brokerages can restrict trading, liquidate positions without consent (if held on margin), or face their own bankruptcy proceedings that tie up your assets.

As Dixon notes from his experience as a major creditor in the Celsius Chapter 11 bankruptcy: “Anybody that’s left Bitcoin on an exchange and received a Bitcoin IOU realises the importance of the ability to self-custody.” When companies fail, Bitcoin IOUs become indistinguishable from the legacy system’s risks—you’re just another unsecured creditor waiting years for partial recovery.

3. The Unsustainable Bitcoin Yield Model

VanEck’s analysis reveals a mathematical problem at the heart of the treasury company model that Dixon’s warnings anticipate: high Bitcoin yields are fundamentally unsustainable due to decreasing returns to scale.

In August 2021, Strategy needed just 2.6 BTC to generate one basis point of Bitcoin yield (BTC per share increase). By May 2025, that figure had ballooned to 58 BTC—a 22x increase. In dollar terms, the capital required rose from $126,000 to $5.5 million for the same unit of yield.

This reflects a fundamental mathematical reality: as Strategy’s Bitcoin base grows, each new BTC contributes less marginal yield, and the capital required to generate yield increases exponentially. Eventually, the model hits a wall where no amount of capital raising can meaningfully increase BTC per share.

What happens then?

Either companies slow their Bitcoin accumulation (disappointing investors who expect perpetual growth), they take on increasingly risky leverage to maintain yield, or they pivot to new strategies—potentially selling Bitcoin.

Dixon warns that this endgame pressure creates conditions for wealth extraction from retail shareholders to Wall Street institutions that understand the game’s terminal dynamics.

4. Forced Selling and Index Delisting Risk

JPMorgan’s November 2025 warning illustrates a systemic vulnerability Dixon identifies: treasury companies are embedded in traditional financial infrastructure in ways that create forced selling risks during stress.

MSCI is considering removing Strategy and other digital asset treasury companies from its equity indices. If this happens, JPMorgan estimates approximately $2.8 billion in forced selling from MSCI indices alone, and $8.8 billion total if other index providers like Russell follow suit.

Nearly $9 billion of Strategy’s stock is held by passive index funds—meaning removal would trigger mechanical selling regardless of fundamentals. Investors in these index funds don’t even know they’re getting Bitcoin exposure, and they have no say in whether to hold during volatility.

Dixon’s framework explains why this matters: when you self-custody Bitcoin, no index committee can force you to sell. No passive fund rebalancing can liquidate your position. You maintain complete sovereignty over your property. Treasury company shareholders lack this sovereignty—their exposure depends on the decisions of index providers, fund managers, and corporate executives.

5. Corporate Governance and Dilution Risk

Strategy’s transformation reveals governance risks that Dixon’s analysis captures. The company has systematically diluted shareholders through massive equity issuances—issuing new shares to buy more Bitcoin on the theory that Bitcoin’s appreciation will make the dilution “accretive.”

This works beautifully in bull markets. When Bitcoin rises faster than share dilution, the Bitcoin-per-share metric improves, and shareholders celebrate.

But what happens in prolonged bear markets or when Bitcoin’s growth slows?

Recent concerns among Strategy investors show the model’s fragility. As one observer noted: “The updated MSTR Equity Guidance could potentially hurt the company by diluting shareholder value, eroding investor confidence, putting downward pressure on the stock price, and increasing financial risk due to dependency on Bitcoin’s volatility.”

Critics like Peter Schiff argue: “Had Saylor bought just about any other asset, MSTR would have been better off.”

While this ignores Bitcoin’s superior long-term performance, it highlights the governance question: shareholders have no control over dilution, debt issuance, or Bitcoin accumulation pace. Management controls everything, and shareholders must trust their judgment indefinitely.

6. Regulatory and Legal Risk

Dixon’s experience with UK regulators attempting to kill his Bitcoin strategy through “Operation Chokepoint 1.0” informs his understanding of regulatory risk to treasury companies.

Bitcoin treasury companies sit at the intersection of securities regulation, cryptocurrency policy, and corporate law. They face potential regulatory actions, including:

- Reclassification as investment companies (triggering different regulatory requirements)

- SEC scrutiny of how they account for Bitcoin holdings

- Tax treatment changes that eliminate current advantages

- Restrictions on debt issuance or equity offerings

- Forced disclosure requirements that compromise operational security

Strategy’s recent wallet exposure illustrates the security implications of regulatory compliance. The company revealed specific wallet addresses holding billions in Bitcoin, potentially making it a target for sophisticated attacks. Self-custody users can maintain privacy about holdings and wallet addresses, reducing security risks.

More fundamentally, Dixon argues that treasury companies validate the debt-based fiat system by providing a bridge for Wall Street money. They become regulatory choke points that governments can pressure during crises—demanding Bitcoin sales, restricting operations, or forcing disclosure in ways that harm shareholders and the broader Bitcoin ecosystem.

7. The Systemic Risk Concentration

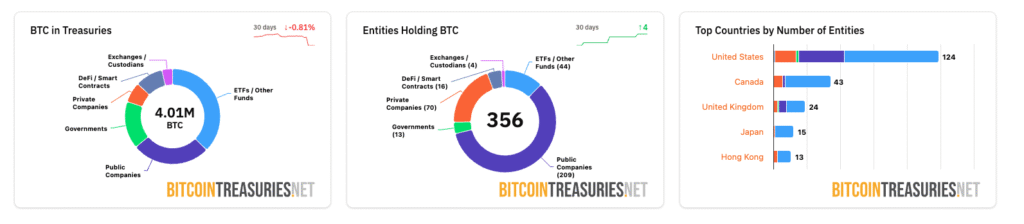

Perhaps Dixon’s most sophisticated concern is about systemic risk concentration. As Bitcoin flows into a small number of very large custodial pools—Strategy’s 649,000 BTC, ETF custodians holding hundreds of thousands more, institutional lenders and miners—the network becomes vulnerable to coordinated attacks or crises.

Dixon warns that BlackRock’s influence within the financial-industrial complex is a key factor. The asset manager has index weight across “20,000 companies,” its Aladdin risk platform is used by numerous large asset managers, and it maintains close ties to policymakers.

The concern is that during a severe crisis, these concentrated custodial pools could become targets for wealth extraction through sophisticated financial engineering. Dixon envisions scenarios where “elaborate schemes to steal your Bitcoin” emerge during liquidity events engineered to seize coins from leveraged or custodial holders.

While large entities cannot permanently manipulate Bitcoin’s price due to fixed supply, Dixon warns, “they can do elaborate schemes to steal your Bitcoin”—through bankruptcy remote structures that favour certain creditors, forced liquidations during manufactured panics, regulatory actions that freeze custodial accounts, or coordinated selling that triggers cascading liquidations.

“Bitcoin is going to be placed at the very, very centre of a future and upcoming currency war,” Dixon argues, asserting that financial-industrial networks will “engineer some kind of pump and dump cycle that resets the chessboard.”

How Net Asset Value (NAV) Works?

The Net Asset Value is essentially the book value per share of a fund or company.

The formula for NAV per share is:

- Total Assets includes the current market value of all investments (like Bitcoin, stocks, bonds, etc.) plus cash and other receivables.

- Total Liabilities includes any money the company owes (like debt, expenses, and payable accounts).

- Total Number of Outstanding Shares is the count of shares currently held by all investors.

For mutual funds, the share price is typically set exactly at the NAV per share at the end of the trading day. However, for publicly traded companies, the stock’s market price can trade at a premium (above NAV) or a discount (below NAV) to its NAV.

The Significance of NAV Dropping Below $1

In the context of a company (like a Bitcoin treasury company) whose primary value comes from its assets, the stock price trading below its NAV per share is a critical signal.

Let’s apply a simplified model where the company’s only major asset is Bitcoin (BTC) and it has minimal liabilities:

When the stock’s market price drops below the value of the NAV per share (i.e., its market capitalisation is less than the value of its BTC treasury), it means the market is effectively valuing the company’s operating business at zero or even a negative value.

If we simplify further and consider a theoretical case where a share’s target value is $1 (perhaps in a money market fund context, but more often applied to asset value per share), a drop below $1 signifies a fundamental loss in the market value of the underlying assets relative to the equity.

Rebalancing with Bitcoin Sales and Stock Buyback

For a Bitcoin treasury company facing a sharp drop in its market price relative to its NAV, the strategy of selling Bitcoin and buying back stock is a defensive measure intended to rebalance the stock price to or above the NAV per share. This process is often called NAV arbitrage or a buyback program.

1. The Trigger

The trigger is when the company’s market share price falls to a significant discount compared to its NAV per share. For simplicity, if we assume an ideal scenario where the NAV per share is $\$1$ and the stock trades at $\$0.80$, the discount is 20%.

The company must act to protect shareholder value.

2. The Bitcoin Sale (Asset Liquidation)

The treasury company will sell a portion of its Bitcoin holdings on the open market. This converts the volatile digital asset (BTC) into stable fiat currency (Cash).

- Effect: This sale provides the necessary cash proceeds for the buyback without needing to raise new capital or take on debt.

3. The Stock Buyback (Equity Reduction)

The company then uses the cash proceeds from the Bitcoin sale to repurchase its own outstanding shares in the open market. These repurchased shares are often retired or held as treasury stock.6

- Impact on NAV per Share: A buyback increases the NAV per share in two ways:

- Reduces the Denominator: The number of Total Outstanding Shares in the NAV formula decreases.

- Forces Convergence: The act of buying back shares creates demand for the stock, putting upward pressure on the market price and pushing it back toward the higher intrinsic NAV per share.7

By reducing the share count with cash raised from selling an equivalent value of Bitcoin, the company can often stabilise or even increase its Bitcoin per share metric, which is a key measure for investors in these types of companies. If all goes according to plan, this rebalancing can re-establish the market’s belief that the company’s stock is a premium way to hold the underlying asset.

Why Self-Custody Is Superior: Dixon’s Framework

Dixon’s prescription is unambiguous: self-custody first, always, without exception. But his argument goes beyond mere security—it’s about maintaining Bitcoin’s fundamental properties and boycotting the systems Bitcoin was created to replace.

Property You Actually Own

The core distinction Dixon draws is between property you own and property you have a claim on. Bitcoin in self-custody is property you own—you control the private keys, you can spend it without permission, you can transmit it without intermediaries, and no third party can seize it, freeze it, or deny you access.

Bitcoin held through treasury companies, ETFs, or custodial platforms is property you have a claim on—legally documented promises that you’re entitled to a certain amount of Bitcoin, contingent on the company remaining solvent, the custodian maintaining security, your brokerage not restricting access, and no regulatory or legal actions interfering.

In Dixon’s framework, claims are not property. “Bitcoin is money you can own,” he emphasises—but only if you actually custody it yourself.

The Skills Everyone Must Develop

Dixon argues that “the skill of self-custody is something everyone has to do,” urging viewers to develop these capabilities now rather than during a crisis.

The essential skills include:

- Key Management: Understanding how to generate, back up, and secure private keys using hardware wallets, multisignature setups, or other cold storage methods.

- Inheritance Planning: Creating systems for family members to access your Bitcoin if something happens to you—without exposing yourself to theft while alive.

- Operational Security: Maintaining privacy about your holdings, avoiding phishing attacks, verifying addresses before sending, and following best practices for transaction security.

- Disciplined Accumulation: Implementing Dixon’s personal rule set of buying on a fixed cadence, avoiding emotional decisions, and thinking in multi-year horizons rather than trading for short-term gains.

Dixon frames this as boycotting the system: “By owning your Bitcoin in self-custody, you remove it from the control of the giant asset managers who want you to hold it in their ETFs, making them even more powerful

The Long-Term Thinking Advantage

Dixon distinguishes between two types of Bitcoin participants: those drawn to short-term gains and those who understand ownership. “True understanding comes from experiencing a disaster and realising the value of owning and controlling your money,” he notes.

Self-custody requires longer time horizons and more discipline than trading treasury company stocks, but it provides:

- No worry about corporate decisions outside your control

- No exposure to leverage cascades or margin calls

- No dependence on custodians maintaining solvency

- No risk of forced selling during index rebalancing

- Complete sovereignty over your wealth

Archie offers a balancing perspective: allocate only capital you can leave untouched for at least four years, and improve quality of life rather than simply “basking in the warmth of your UTXOs” indefinitely. But within those parameters, self-custody provides security that treasury companies can never match.

The Moral and Philosophical Dimension

For Dixon, Bitcoin self-custody transcends financial calculation—it’s a moral stance against the “Proof of Weapons Network” (P.O.W.N.) that he argues controls the fiat monetary system.

Dixon’s framework posits that every fiat currency unit is created through debt, enriching banks and institutions while impoverishing ordinary people through inflation. “The entire fiat currency system is inherently immoral and unethical. It’s not broken; it’s working perfectly as designed to enrich the few.”

Bitcoin represents an opt-out—but only if you self-custody. Holding Bitcoin through treasury companies or ETFs “validates the debt-based fiat system by providing a bridge for Wall Street money,” undermining Bitcoin’s revolutionary potential.

Dixon advocates for three boycotts:

- Boycott BlackRock: By owning Bitcoin in self-custody, you remove it from control of giant asset managers who want you to hold it in their ETFs.

- Boycott the Banks: By accumulating enough Bitcoin that you don’t need to borrow, you starve banks of their power, since debt is the grease that runs the engine of the Proof-of-Weapons Network.

- Boycott the War Machine: By becoming conscious of how you spend money, you can support local communities and decentralised systems while defunding corporations profiting from crimes against humanity.

This philosophical framework explains Dixon’s urgency: treasury companies aren’t just financially suboptimal—they’re ideologically incompatible with Bitcoin’s purpose.

The Counterarguments: Are Treasury Companies Really That Dangerous?

Dixon’s warnings are stark, but not everyone in the Bitcoin community shares his concerns. Several counterarguments deserve consideration:

The Accessibility Argument

Many argue that custodial solutions and treasury companies are necessary bridges for broader adoption. For average consumers, managing private keys and securing digital assets can be daunting. Treasury companies and ETFs offer a regulated, familiar entry point that brings capital and legitimacy to Bitcoin.

As one analysis notes: “Custodial services offer a bridge for those who want to invest in Bitcoin without delving into the complexities of self-custody.”

The Institutional Legitimacy Argument

Institutional involvement brings not only capital but also regulatory compliance that could safeguard the market against fraud and manipulation. The presence of established firms like BlackRock, Fidelity, and traditional financial institutions provides insurance, regulatory oversight, and professional risk management.

From this perspective, institutional custody reduces certain risks (theft, loss, operational errors) even while introducing counterparty risk.

The Leverage Is Transparent Argument

Defenders of treasury companies emphasise transparency. Unlike the opaque rehypothecation and margin lending that destroyed Celsius and FTX, treasury company debt is public, long-dated, and structured conservatively. Michael Saylor claims Strategy is “engineered to survive an 80-90% drawdown,” with leverage currently at “10 to 15% and trending toward zero.”

“So, I think we’re pretty indestructible,” Saylor states confidently.

The False Choice Argument

Some argue that Dixon presents a false binary. Why not both institutional products for mainstream adoption and self-custody for sovereignty-focused users? Bitcoin can serve multiple use cases simultaneously, and different investors have different risk tolerances and priorities.

Now you can hold that opinion, or you can HODL that opinion by putting your money where your mouth is, leave it with a custodian or secure it in self-custody and see which one proves to be the more fruitful approach over the coming decade.

Evaluating the Evidence: What Recent Events Show

Recent market developments provide real-world tests of Dixon’s warnings versus counterarguments:

- Strategy’s Recent Volatility: The stock falling 40% while Bitcoin declined modestly validates concerns about leverage amplification. Treasury companies do magnify volatility in both directions, exposing shareholders to losses exceeding Bitcoin’s movements.

- JPMorgan’s Delisting Warning: The revelation that $8.8 billion in forced selling could result from index exclusion proves that treasury company shareholders lack sovereignty. Passive fund holders are experiencing Bitcoin exposure they didn’t choose and can’t control.

- Unsustainable Yield Mathematics: VanEck’s analysis showing Strategy needs 22x more Bitcoin to generate the same yield as 2021 validates Dixon’s concerns about the model’s long-term sustainability. Eventually, growth must slow or leverage must increase.

- Security Exposure Risks: Strategy’s public wallet addresses becoming known raises operational security concerns that self-custody users can avoid. As Dixon notes from his blockchain expertise, transparency requirements create vulnerabilities.

- Bear Market Resilience Unknown: Strategy’s model has never been tested in a prolonged Bitcoin bear market (2+ years of declining prices). The 2022 crash was brief, and Bitcoin recovered quickly. Whether the leverage and dilution model survives a multi-year drawdown remains unknown.

The Bitcoin Personal Investment Strategy

If you find Dixon’s arguments compelling and you want to de-risk from all of the above, the tried and tested approach forged across multiple Bitcoin cycles is one you should look to execute on:

- Buy on a Fixed Cadence: Dollar-cost average by purchasing Bitcoin regularly regardless of price (weekly, monthly, quarterly). This eliminates timing risk and removes emotional decision-making.

- Hold Coins in Self-Custody: Use hardware wallets, multisignature setups, or other secure self-custody solutions. Never leave Bitcoin on exchanges or in custodial accounts except briefly during purchases.

- Think in Multi-Year Horizons: Evaluate Bitcoin investments over 4+ year periods, not days, weeks, or months. This long-term perspective allows you to weather volatility without panic selling.

- Develop Self-Custody Skills Now: Learn key management, inheritance planning, and operational security during calm periods—not during crises when mistakes are costly.

- Accumulate Enough to Not Need Borrowing: Rather than using leverage or borrowing against Bitcoin, accumulate enough that you don’t need to sell or borrow to meet financial needs. This eliminates liquidation risk entirely.

You Can Survive A Bear Market, You Can’t Survive A Bear Trap

Simon Dixon describes Bitcoin’s current moment as a fork—not in the code, but in the community. “A real tension is building as traditional financial players from the Proof-of-Weapons Network enter our ecosystem.”

On one side are those who see Bitcoin as “number go up technology“—a way to outperform the Fed and generate leveraged returns through treasury companies, ETFs, and sophisticated financial products.

On the other side are those who remember Bitcoin’s purpose:

“Bitcoin was designed as a tool to boycott and escape the corrupt banking system. It’s a way to own your money without a bank, spend it without government permission, and have a monetary policy that can’t be manipulated by central bankers.”

Dixon argues these visions are incompatible:

“I will no longer spend my time on X Spaces hosted by people who are happy to make the institutions of the Proof-of-Weapons Network more powerful.”

The risks he identifies in Bitcoin treasury companies are not theoretical—they’re materialising in real time through volatility amplification, forced selling risks, unsustainable yield dynamics, counterparty dependencies, and systemic concentration. Whether these risks reach crisis proportions or remain manageable inconveniences remains to be seen.

But Dixon’s prescription is clear:

“Vote with your money and make sure you are securing the only property you can truly own: Bitcoin in self-custody.”

Treasury companies offer convenience and leverage at the cost of sovereignty. ETFs provide accessibility at the expense of ownership. Custodial platforms promise security while introducing counterparty risk. These tradeoffs may be acceptable for some users in some circumstances—but only if entered into with full awareness of what’s being surrendered.

“Everybody has to do it,” Dixon emphasises about self-custody skills. “The skill of self-custody is something everyone has to do.”

The Wall Street attack phase Dixon warns about may or may not unfold as he predicts. BlackRock and other institutions may prove to be responsible stewards of Bitcoin rather than predatory extractors of wealth. Treasury companies may mature into sustainable business models rather than leverage-fueled bubbles awaiting catastrophic collapse.

But here’s what’s undeniable: When you self-custody Bitcoin, you eliminate every risk Dixon identifies. No counterparty can fail. No CEO can make bad decisions with your coins. No margin call can liquidate your position. No index committee can force you to sell. No custodian can get hacked. No bankruptcy proceeding can freeze your assets.

You own Bitcoin. Not a share of a company that owns Bitcoin. Not a claim on Bitcoin. Not an IOU. Actual Bitcoin that you control with your private keys.